Diversification

The first step in establishing a good trading methodology Part II starts with optimising risk exposure using:

- A portfolio between 4-10 of uncorrelated and risk-adjusted assets; or

- A portfolio of 3 to 5 uncorrelated trading systems; or

- Both 1 and 2 working together.

The advantage of a diversified portfolio

The benefit of having a diversified portfolio of assets is it smooths out the equity curve and get a substantial reduction in the total drawdown. I’ve experienced myself the psychological advantage of having an extensive portfolio, especially when volatility is high.

Losing 10% on an asset is very hard. But if you had spread the risk into five assets and got four winners at the same time, then that 10% loss becomes an acceptable 2% loss in the overall five-asset account that will be compensated with, maybe, 4-6% profits on other securities. That, I can assure you, gave me the strength to follow my system!.

Several trading systems in tandem

The advantage of 3 or more trading systems in tandem is twofold. It helps, also improving overall drawdown and smooth the equity curve, because we distribute the risk between the systems. It also helps to raise profits, since every system contributes to profits in good times and fill the loss the underperforming is doing.

That doesn’t work all the time. There are days when all your assets tank, but, overall, a diversified portfolio together with a diversified catalogue of strategies is a peacemaker for your soul.

The math of diversification

As an example, below is the equation of the risk of an n-asset portfolio when there’s no correlation:

𝜎 = √(w1𝜎12+ w2𝜎22+ … + wn𝜎n2)

where 𝜎i is the risk on an asset and wi is the weight of that asset in the basket.

Let’s assume that we hold a basket of equal risk-adjusted positions in 5 uncorrelated markets with a total risk of $10. Therefore, we have a $2 risk exposure on each market, and the total correlated risk would have been $10. However, if the assets were completely uncorrelated, the expected combined risk would be computed using the above equation.

Then:

𝜎 = √(5 x 22) = √20 = 4.47

So, for the same total market exposure, we have reduced our risk by more than 50%.

Correlation in the real world

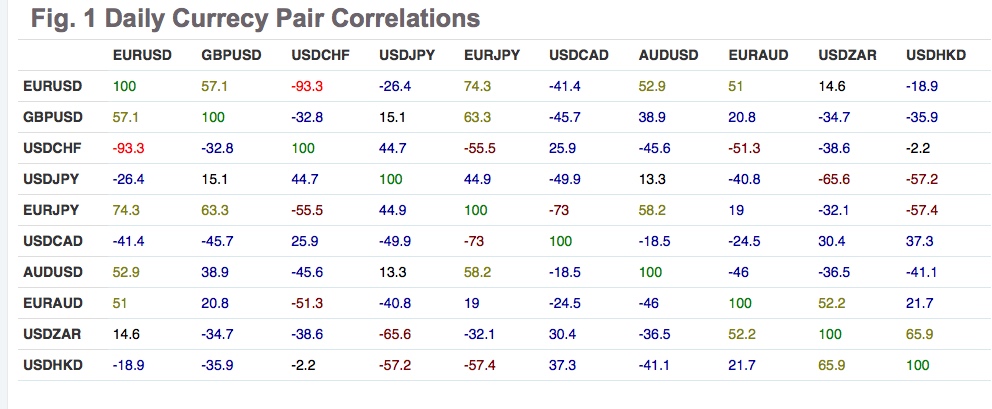

Expecting zero correlation in markets is not realistic, but the idea is to try to minimise it, or even, use negatively correlated trades, so one sharp movement against us can be counteracted with a sharp move in the other trade.

Correlation on Forex Pairs

One final tip: Try to standardise the volatility on your trades. This powerful idea tries to adapt the size of the position to the expected volatility of the asset, trying to equate the risk on all open positions.

You should, also, plan for a maximum daily loss. For example, you may decide that you will use four $100 risk bullets for the day, which makes it a total $400 daily loss. If you hit that loss, you stop trading real money that day and just do paper trades until the next day. This also applies for the maximum number of consequtive bets, in this case four.

On part III we will deal with the track record.

Take your trading to the next level with our 14 Day, No Obligation, Free Trial. You will soon discover why we are trading’s best-kept secret. We are successfully building the world’s largest group of profitable traders and would like you to be part of it.

You can join for as little as $19.99 per month, no contract, cancel anytime. This amount can be covered with just one profitable trade with us per month, the rest is pure profit. You will benefit from unparalleled access to our professional traders, our transparent trading performance, our LiveTradeRooms and access to the most comprehensive trading education on the market. What have you got to lose? JUST CLICK HERE TO GET STARTED NOW and see how real money is made!